You’ve spent years building your corpus. Now you want that money to come back to you — regularly, predictably, without selling everything at once.

That’s exactly what an SWP (Systematic Withdrawal Plan) does.

Whether you’re a retiree in Ahmedabad looking for monthly income, a parent funding a child’s college fees, or simply someone who wants to replace a low-yield FD — SWP is one of the most practical and tax-efficient tools in mutual fund investing.

In this guide, we break down everything you need to know: what an SWP is, how it works step by step, the real numbers, tax implications in 2026, and when it makes sense for you.

What is an SWP (Systematic Withdrawal Plan)?

An SWP, or Systematic Withdrawal Plan, is a facility in mutual funds that allows you to withdraw a fixed amount of money at regular intervals — monthly, quarterly, or annually — while keeping the remaining investment active and compounding.

Think of it as the reverse of an SIP. With an SIP, you invest a fixed amount regularly. With an SWP, you withdraw a fixed amount regularly.

Simple definition: You invest a lump sum in a mutual fund. You instruct the fund house to credit ₹10,000 (or whatever amount you choose) to your bank account every month. The fund redeems just enough units to pay you that amount. The rest stays invested and keeps growing.

SWP is not a new product. It is a feature available on almost every mutual fund scheme in India — from equity funds to hybrid funds to debt funds.

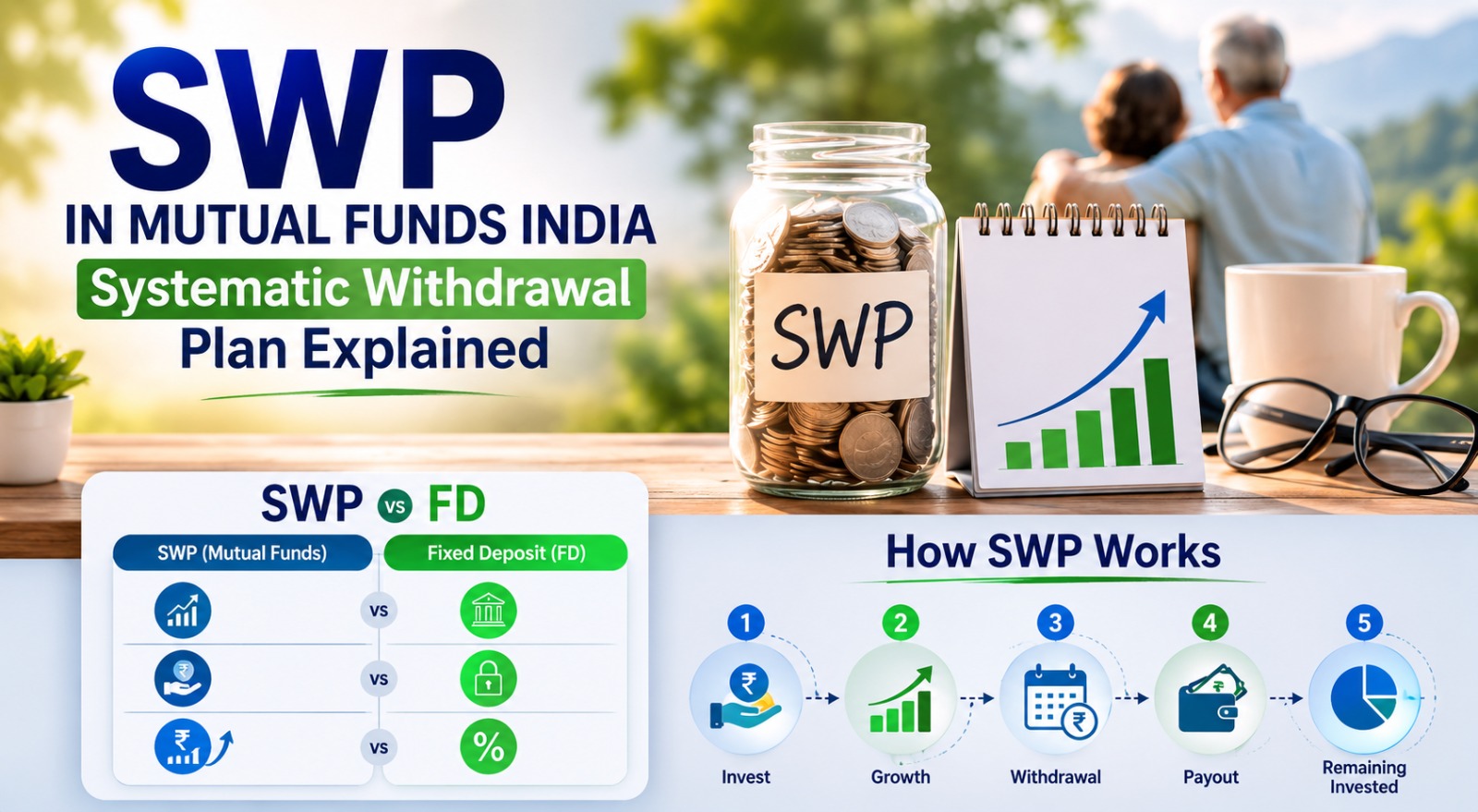

How Does an SWP Work? (Step-by-Step)

Here’s exactly what happens behind the scenes every month when your SWP runs:

Step 1 — You invest a lump sum

You invest, say, ₹25 lakh in a mutual fund of your choice. This gets converted into units at the current NAV (Net Asset Value).

Step 2 — You set up the SWP

You decide:

- How much to withdraw (e.g., ₹15,000/month)

- How often (monthly, quarterly)

- The start date

- The duration (fixed period or ongoing)

Step 3 — Units are redeemed automatically

On your chosen date each month, the fund calculates how many units need to be sold to give you ₹15,000. If the NAV is ₹50, it redeems 300 units. If the NAV has risen to ₹60 next month, only 250 units are redeemed.

Step 4 — Money hits your bank account

The proceeds are directly credited to your registered bank account — no manual action needed.

Step 5 — The rest keeps compounding

The remaining units stay in the fund, continue to grow with the market, and fund future withdrawals.

SWP Example with Real Numbers

Let’s say Rameshbhai, a 58-year-old retired professional from Ahmedabad, invests ₹30 lakh in a balanced advantage fund and sets up an SWP of ₹20,000 per month.

| Month | Opening Value | NAV | Units Redeemed | Withdrawal | Closing Value |

|---|---|---|---|---|---|

| 1 | ₹30,00,000 | ₹100 | 200 | ₹20,000 | ₹29,80,000 |

| 2 | ₹30,14,000* | ₹101 | 198 | ₹20,000 | ₹29,94,000 |

| 3 | ₹30,50,000* | ₹103 | 194 | ₹20,000 | ₹30,30,000 |

*Assuming fund grows at ~10% annualised

When the fund’s growth rate exceeds the withdrawal rate, the corpus actually grows over time — even while you’re drawing income. This is the magic of SWP done right.

Types of SWP

1. Fixed Amount SWP

You withdraw a fixed rupee amount every month. Most commonly used. Best suited for predictable expenses like rent, EMIs, or household costs.

2. Appreciation-Based SWP

You withdraw only the gains earned on your investment, keeping the principal intact. Ideal for investors who want income without eroding the original corpus.

3. Variable SWP

You can increase or decrease the withdrawal amount based on your financial needs. Offers maximum flexibility.

SWP vs FD — Which is Better?

This is the question every investor in Gujarat eventually asks. Here’s an honest comparison:

| Feature | SWP (Equity/Hybrid Fund) | Bank FD |

|---|---|---|

| Monthly Income | Yes | Yes (if cumulative, only at maturity) |

| Effective Return | 10–12% p.a. (historical) | 6.5–7.5% p.a. |

| Inflation Protection | Yes (equity component) | No |

| Tax on ₹10L corpus income | ~Nil (LTCG exemption) | As per income slab (up to 30%) |

| Flexibility | High | Low (penalties on premature exit) |

| Capital Protection | Market-linked | Yes (up to ₹5L DICGC) |

| Corpus Growth | Possible | Unlikely after withdrawals |

For most investors above the 20% tax bracket, SWP from an equity-oriented hybrid fund is significantly more tax-efficient than a bank FD.

SWP Tax Rules in 2026 — What You Need to Know

This is where most people get confused. Let’s keep it simple.

Every SWP withdrawal is a redemption of units. It is taxed as capital gains — not as income.

The FIFO (First In, First Out) rule applies: The oldest units in your portfolio are redeemed first.

For Equity-Oriented Funds (≥65% in equities):

- Units held > 12 months → LTCG (Long-Term Capital Gains)

Tax rate: 12.5% on gains above ₹1.25 lakh per year (Budget 2024 rate, unchanged in 2026)

The first ₹1.25 lakh of annual LTCG is completely tax-free. - Units held ≤ 12 months → STCG (Short-Term Capital Gains)

Tax rate: 20% flat

Key insight: Only the gain portion of each withdrawal is taxed — not the entire withdrawal amount. If you withdraw ₹15,000 but only ₹3,000 is gain, you’re taxed on ₹3,000 only.

For Debt Funds (purchased after April 1, 2023):

All gains — regardless of holding period — are taxed at your income slab rate. No indexation benefit.

Practical Tax Example

Rameshbhai withdraws ₹2.4 lakh over 12 months via SWP from a hybrid equity fund. His total gains from these withdrawals = ₹60,000. Since ₹60,000 < ₹1.25 lakh annual LTCG exemption, his tax on SWP income = ₹0.

Compare that to the same ₹2.4 lakh from an FD taxed at 30% slab — he’d pay ₹72,000 in tax.

Who Should Use an SWP?

SWP is particularly well-suited for:

Retirees seeking monthly income

Replace pension or FD income with a tax-efficient, inflation-beating withdrawal stream.

Parents funding education expenses

Set up a quarterly SWP to fund college tuition without selling your entire corpus at once.

Professionals supplementing salary

Use an SWP to fund EMIs or business expenses during lean months.

NRI investors with India corpus

SWP proceeds can be credited to NRE/NRO accounts for easy repatriation (subject to applicable TDS for NRIs).

Anyone exiting an FD mindset

If you’re sitting on a large FD renewing every year and paying 30% tax on interest, an SWP migration plan may significantly improve your post-tax income.

Which Mutual Funds Are Best for SWP?

Not all mutual funds are equally suited for SWP. Here’s a general framework:

For stability + income (low to moderate risk):

Balanced Advantage Funds / Dynamic Asset Allocation Funds — these automatically rebalance between equity and debt, reducing volatility in your corpus.

For higher growth + long horizon:

Equity hybrid funds or large-cap equity funds — suitable if your corpus is large and you’re drawing less than 6–7% annually.

For short-term or conservative needs:

Arbitrage funds or conservative hybrid funds — these offer predictable, low-volatility returns, ideal for 1–3 year SWP goals.

Want personalised fund recommendations for your SWP? Our team at Aarav Investments analyses your corpus, risk profile, and tax situation before suggesting a fund.

How to Start an SWP — 4 Simple Steps

- Choose the right fund — based on your risk appetite, corpus size, and withdrawal goal

- Invest the lump sum — online through your existing mutual fund account or through a distributor

- Register the SWP — specify amount, frequency, and start date

- Track annually — review the corpus every year to ensure withdrawals are sustainable

Common SWP Mistakes to Avoid

Withdrawing too aggressively

If your withdrawal rate (annual withdrawal ÷ corpus) exceeds the fund’s long-term return, your corpus will shrink and eventually run out. A safe withdrawal rate is typically 6–8% of corpus per year.

Choosing the wrong fund

High-risk sector or small-cap funds are not suitable for SWP — volatility can devastate your corpus if markets fall during withdrawals.

Ignoring exit loads

Some funds charge an exit load (typically 1%) on units redeemed within 12 months. Plan your SWP start date to avoid this.

Not reviewing annually

Markets change. Your corpus changes. Review your SWP every financial year to ensure the plan remains on track.

SWP vs IDCW Option — What’s the Difference?

Many investors confuse SWP with the IDCW (Income Distribution cum Capital Withdrawal) option of mutual funds. They are different.

| SWP | IDCW | |

|---|---|---|

| Amount control | You decide | Fund declares (variable) |

| Tax | Capital gains (often lower) | Taxed as income at slab rate + 10% TDS above ₹10,000 |

| Corpus impact | Controlled | Can reduce NAV significantly |

| Predictability | High | Low |

SWP is almost always more tax-efficient and more predictable than the IDCW option.

Frequently Asked Questions (FAQ)

Q: Can I stop or modify my SWP?

Yes. You can pause, modify, or stop your SWP anytime — there’s no lock-in or penalty (except exit loads if applicable).

Q: Is SWP safe?

SWP from a well-diversified equity or hybrid mutual fund is considered a low-to-moderate risk strategy, especially when the withdrawal rate is conservative (below 7% annually). The underlying fund carries market risk.

Q: What is the minimum amount for SWP?

Most fund houses allow SWP of as low as ₹500–₹1,000 per month, though practically, SWPs make most sense for corpus sizes above ₹5–10 lakh.

Q: Can NRIs use SWP?

Yes. NRIs can invest in Indian mutual funds and use the SWP facility. Withdrawals are subject to TDS at applicable NRI rates (20% for equity STCG, 12.5% for LTCG). They can file for a refund if TDS is over-collected.

Q: Is SWP better than a pension plan?

SWP offers more flexibility and potentially higher returns than most traditional pension plans, but lacks the guaranteed income of an annuity. Many financial advisors recommend a combination of both.

Final Word: Is SWP Right for You?

SWP is not a magic formula — it’s a disciplined strategy that works best when paired with the right fund, the right withdrawal rate, and regular annual reviews.

Done right, SWP can give you monthly income that is more tax-efficient than an FD, potentially inflation-beating, and completely under your control.

At Aarav Investments, we’ve helped hundreds of families in Ahmedabad — from working professionals in Bopal to retired couples near Shyamal Circle — set up SWPs that are tailored to their life stage, risk appetite, and tax profile.

If you’re looking for best SWP advisor in Ahmedabad, Gujarat or want to migrate an existing FD corpus into a better structure, let’s talk.

📞 Call / WhatsApp: +91 79907 44040

📧 Email: info@aaravinvestments.in

🏢 Office: 511 Sun Avenue One, Near Shyamal Cross Roads, Ahmedabad – 380015 Location

🌐 Website: aaravinvestments.in

Aarav Investments is an AMFI-registered Mutual Fund Distributor with ARN – 264373. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

Leave a Reply