A recent Income Tax Appellate Tribunal (ITAT) ruling has become one of the most talked-about cases in Indian personal finance circles — and for good reason.

A Singapore-based NRI earned approximately ₹1.35 crore from Indian mutual fund investments and legally paid zero tax in India. No loophole. No evasion. Just smart, lawful financial planning under the India–Singapore Double Taxation Avoidance Agreement (DTAA).

If you are an NRI investing in India — or a resident investor with growing wealth — this case has important lessons for you.

What Happened in the Singapore NRI ITAT Case?

The investor, an NRI residing in Singapore, had invested in Indian mutual funds over time. After redeeming those units, she generated capital gains of close to ₹1.35 crore.

Ordinarily, capital gains from Indian mutual funds are taxable in India. However, she claimed benefits under the India–Singapore DTAA (Double Taxation Avoidance Agreement), arguing that since she was a Singapore tax resident, India did not hold the right to tax those gains.

The Income Tax Department challenged this claim. The case went to ITAT — and the tribunal ruled in favour of the NRI investor.

How Did She Pay Zero Tax Legally?

India has bilateral tax treaties with several countries designed to prevent the same income from being taxed twice. These treaties define which country holds taxation rights when income crosses borders.

Under the India–Singapore DTAA provisions applicable to this case:

- The investor held valid Singapore tax residency

- The capital gains were taxable as per Singapore’s tax laws

- Singapore does not levy capital gains tax

Result: India could not tax the gains due to treaty protection. Singapore did not tax them either. Legal zero tax.

This is not a loophole — it is exactly how international tax treaties are designed to work.

Does This Mean Every NRI Can Avoid Tax in India?

No — and this is where many investors get misled by social media headlines.

Tax liability for NRIs investing in India depends on multiple factors:

- Country of residence — Each country has a different DTAA with India

- Type of DTAA provisions — Not every treaty offers the same benefits

- Mutual fund category — Equity vs debt vs hybrid funds are taxed differently

- Holding period — Short-term vs long-term capital gains rules apply

- Residential status — NRI vs RNOR vs Resident Indian classification matters

- Proper documentation — A valid Tax Residency Certificate (TRC) is mandatory to claim DTAA benefits

Without the right documents and proper planning, claiming DTAA benefits can be denied — and penalties can follow.

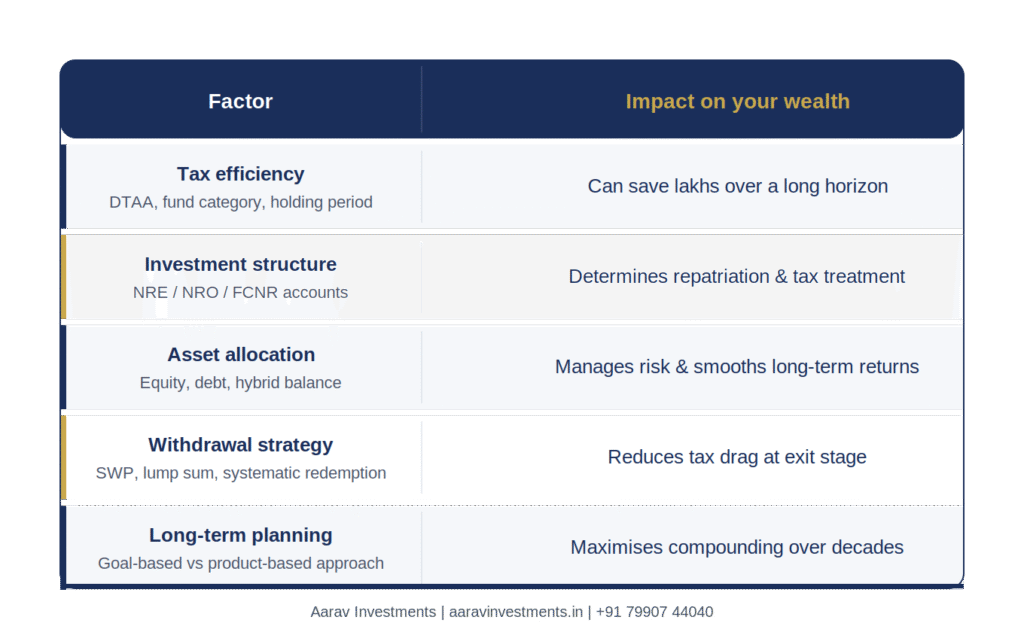

Why Tax Planning Is as Important as Fund Selection

This case makes one thing absolutely clear: building wealth is not just about picking the right mutual fund.

Two NRI investors with identical portfolios and identical returns can end up with very different post-tax wealth — purely because of how their investments are structured.

Factors that determine your actual returns:

For NRIs based in the UK, Germany, USA, Singapore, or the Gulf, each jurisdiction has its own tax treaty with India. The planning approach must be customised, not copy-pasted.

Key Lessons for Indian Investors (NRI and Resident)

Even if you are a resident Indian, this case holds lessons worth applying:

1. Understand Tax Before You Invest

Taxes can erode a significant portion of your returns if not planned for. Before investing, ask: How will this be taxed when I redeem?

2. Mutual Fund Category Matters

Equity funds, debt funds, hybrid funds, and international funds each carry different tax rules. Choosing based only on past returns without considering tax impact is a common and costly mistake.

3. Documentation Is Half the Battle

For NRIs, maintaining proper documentation — Tax Residency Certificate, NRE/NRO account records, PAN, KYC — is essential before claiming any DTAA benefit.

4. Professional Guidance Pays for Itself

As your investment portfolio grows, financial decisions become more complex. An experienced mutual fund advisor does not just recommend schemes — they help you build a tax-efficient, goal-aligned strategy that stands up to scrutiny.

NRI Investment Planning in Ahmedabad — Aarav Investments

At Aarav Investments, we specialise in helping NRI clients from across the world — including the UK, Germany, Singapore, USA, and Gulf countries — invest wisely in India.

We are an AMFI-registered Mutual Fund Distributor based in Ahmedabad, with over a decade of experience serving NRI families and High Net-Worth investors.

Our NRI investment services include:

- NRI mutual fund investment planning — NRE/NRO/FCNR-based strategies

- DTAA-compliant investment structuring — coordinated with your CA or tax consultant

- Goal-based portfolio management — retirement, child education, property purchase

- SIP and lump sum strategies — tailored to your income cycle and country of residence

- GIFT City investment options for UK and European NRIs

- NPS and insurance advisory for NRIs building long-term India exposure

Whether you are just starting your India investment journey or reviewing an existing portfolio, we provide the clarity and structure your wealth deserves.

📍 Office: 511 Sun Avenue One, Near Shyamal Cross Roads, Ahmedabad – 380015

📞 Call/WhatsApp: +91 79907 44040

📧 Email: info@aaravinvestments.in

🌐 Website: aaravinvestments.in

Conclusion

The Singapore NRI ITAT case is not a story about tax avoidance. It is a story about informed, compliant, and well-structured financial planning.

Smart investors — whether NRI or resident — focus not just on earning higher returns, but on keeping more of what they earn through tax-efficient strategies.

If you are an NRI looking for a trusted investment advisor in Ahmedabad, or a resident investor wanting to understand how to make your mutual fund portfolio more efficient — we are here to help.

Book a Free Consultation with Aarav Investments →

Disclaimer: This blog is for educational purposes only and does not constitute tax or legal advice. Tax laws and DTAA provisions change from time to time. Please consult a qualified tax advisor and your investment advisor for guidance specific to your situation.

Leave a Reply